Many students of economics may have studied about the IS-LM model, and then tackled with various homework assignments requiring to solve the excessively complex formulas and understand the theoretical reasoning behind them. These macroeconomic teachers always expect students to consume their precious time and energy to solve a ton of equations and memorise the theory to explain what these algebras denote. The mathematical formulas applied to this model are mostly linear and straightforwardly simple but all equations are interconnected to all the others. As long as they are familiar with economics in general, it should not be a big problem to understand the theoretical bases. But, these teachers require these students to interlink all the necessary theories which textbooks show to all equations. In addition, when the interpretation of these students differ from what the textbooks and the teachers expect, their mark tends to be lowered. Therefore, studying the IS-LM model is very exhausting.

Nevertheless, despite their efforts and well-understanding, there is a big scepticism about the IS-LM model. There are still many debates about whether or not this model successfully explain the real world economy. Of course, there is always a residual gap between what the prediction model estimates and what the real world phenomenon is in real. This is why the IS-LM model is a problem because of its complex tangle of a bunch of the equations. Especially in social science, when many mathematical equations are used and interlinked together, the total sum of the residuals tends to be significantly magnified, and the bias and the inconsistency of the model also tend to take place much often. Furthermore, these estimate mathematical models are not statistically tested as their formulas are merely based on the literature of economic theories. Therefore, it is really a natural fact that the IS-LM model often fails to fit into what really happens in real.

Even in the pure literature based economic theories and the logical economic theories also counter to the IS-LM model. This report introduces some significant counter-arguments against the IS-LM model as follows.

1. The Ricardian Equivalence

This theory implies that providing economic agents with extra income by the stimulus package does not successfully induce them to spend enough to stimulate their economy. When they prefer consuming/invest less and saving more at the present time to the extra consumption&investment, the extra income available by the tax cut and/or the government expenditure rather causes the negative impact on economy than the positive impact. The cost incurred by the tax cut and/or the government expenditure at the present time period has to be paid back in the future. As the economic stimulus becomes unsuccessful due to their preference of spending less than expected, the tax revenue in the future time period is lowered meanwhile the cost remains.

Those who disagree with the Ricardian Equilibrium argue that there are many economic agents with the low income insufficient to satisfy their needs and wants during the recessionary period so that they happily spend their extra income provided by the stimulus package to stimulate economy.

However, their extra income spent for consumption/investment is eventually transferred to owners of the means of production who produce the consumptions and own the assets invested. These owners will rather want to shift their income earnt from their capital investment to their assets in this downward market to either saving in their bank account or investing more active foreign markets.

When an economy become at the point that even these owners of the means of production become deprived enough to cling to the extra income provided by the stimulus package, the national government is less likely to be able to issue their bonds to incur the debt as the bond credibility is substantially lowered.

2. Liquidity Trap

The stimulus package by the monetary policy channel still does not work due to the liquidity trap. As mentioned in the Ricardian Equivalence, economic agents tend to be reluctant to spend their extra income available during the recession. Even the monetary policy is less likely to incur the cost like the previously mentioned fiscal policy channel, the result is identical to the previously mentioned scenario.

This phenomenon is explained as the liquidity trap. As shown in the graph above, although the extra money supply becomes available to transform to the extra income available for economic agents to spend, the effect is substantially low or even nothing under a very low liquidity level i.e. the investment motive is very low. The little effect on the interest rate reveals little impact of the money supply increase on economy. This means that the factors determining the interest rate such as the price indices, the business activity rate, and the value of this money currency in the foreign currency exchange market hardly changed by this monetary policy.

On the other hand, this interest rate shown in this LM graph merely implies the central bank interest rate, and this only partially affect on the banks' interest rate setting for their borrowers. The rest of this report explains the effect on these interest rates. The IS-LM model neglects explaining the following factors because the IS-LM model assumes all these factors are positively correlated to what it indicates in the model. Nonetheless, the more real economy is obviously different from this false assumption.

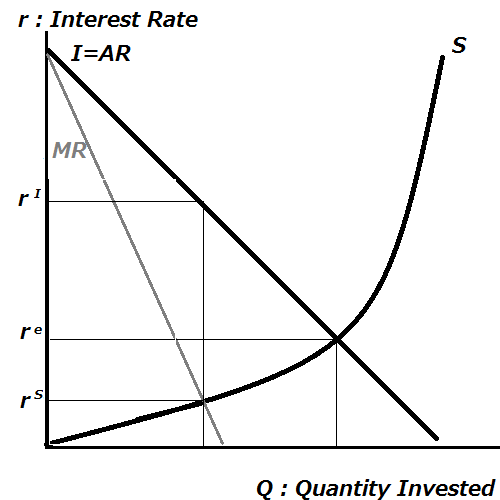

3. Under the Banking Monopoly in case of Risk Neutral

The supporters of the IS-LM model assume that their margin rate tends to be always positively correlated to the central bank interest rate so that the final interest rate for both investment and saving is always controlled by the central bank interest rate affected by the fiscal and monetary policy.

The IS-LM model is based on the assumption that all or majority of private banks and the other financial institutes are under the perfectly competitive market. By contrast, the real world economic situation is even not close to this assumption and actually far away from it. They are in the less competitive market due to the nature of the financial industry and market.

The interest rate is the price of money rent and borrowed. So, the private banks and the other financial institutes need to add the extra rate on the central bank interest rate after borrowing from the central bank to rend their money to their customers in order to compensate for the renders' service cost and reward.

Also, in a market economy, the characteristics and the quality of the financial service is heterogeneous to each other, and the demand is severely affected by their geographical situations e.g. access to customers and clients (both quantitative and qualitative), cultural attitudes toward finance, and the infrastructure for obtaining information and technology available there.

On the top of the service quality issue, the service users are difficult to change their service providers often as much as the mainstream economists assume due to the contract binding them together and the transaction cost to close and open their bank accounts. So, these service users are more likely to be bound to their already contracted financial services.

All in all, the market nature is far more monopolistic owing to these aspects. Then, the interest rates are set at the quantity of money invested where the marginal revenue becomes equal to the cost which is the interest payment for savers for this case. So, the quantity invested is lower than the quantity at the investment and saving intersection, and the interest rate charge for borrowing is always significantly way higher than the interest rate payment for savers.

The interest rate payment for savers may be affected by rise of the central bank interest rate increase but not often by fall of the central bank interest rate unless the market is very competitive. These financial service providers take advantage of this situation so that the interest rate payment for savers often tend to be notably lower than the interest rate charge to borrowers.

The following charts explain the different situations to set the final interest rates.

3.1. When the Central Bank Interest Rate is high

When the central bank interest rate is high, then the interest rate paid to savers is adjusted to be equal to the central bank interest rate.

The quantity of money invested is adjusted to the point where the marginal revenue from the return from investment intersects with the central bank interest rate, and then the interest rate charged for investment becomes higher as the central bank interest rate becomes higher.

3.2. When the Central Bank Interest Rate is low

When the central bank interest rate is low enough to be able to split from the investors' profit margin, then no change of both interest rates tends to take place as shown in the graph above.

This aspect completely contradicts what the IS-LM model assumes. As the market is less competitive, the monopoly power is stronger enough to maintain their high interest charge for investment payment unchanged.

3.3. The extreme case: The Central Bank Interest Rate is either zero or minus

In this extreme case which seems to occur frequently under the world economic crisis period nowadays, many central banks of this world have set their interest rate notably close to zero. Even some claim that they should set the rate zero.

Nonetheless, as shown in the previously mentioned mechanisms, the previously mentioned interest rate setting under the low liquidity, the money supply offered by the central bank with a sizably low interest rate hardly stimulates economy.

The interest payment for savers cannot be set below zero because they will no longer save in these banks or any other financial institutes setting such a negative interest rate.

4. Risk Taking Patterns

On the top of the gap between the interest rates, the IS-LM model over-simplifies the investment pattern influenced by the psychological characteristics of banks, investors, and other financial administrators.

What should be concerned is that the interest rate setting based on the investment volume is not always counter-cyclical to the business cycle, and not all economic agents are risk neutral as many mainstream macro-economists tend to assume.

The following examples are based on the situation of the fiscal and monetary policy is tightened to repress the economic boom or the recession repressing the aggregate income level.

The Y_t denotes the aggregate income invested to economy by these investors, and X_t denotes the investment safety (A higher value indicates the lower investment risk).

4.1 Risk Neutral: The IS-LM Curve assumes all agents are as such

This is the way which the risk neutral agents regularly react to the business cycle downturn causing the aggregate income shrinking.

They simply reduce the investment volume, and passively react to the investment risk change.

The IS-LM model may work as long as all the economic agents act as such.

4.2. Risk Averse

The risk averse economic agents put priority on their investment safety to their nominal income gain from their investment volume.

When their investment opportunity becomes more limited, they tend to take this situation warning of losing their business opportunity and potential collapse of their investing clients.

Even in the case where the fiscal and monetary policy represses the booming economy, they imagine about the negative side effect of the over-expansion which the policy alerts, and then they prefer preparing for the worst case scenario.

In particular during the recession, more agents tend to become the risk averse because their perspective tends to be more pessimistic about the future.

All in all, the income downturn exaggerates the investment discouragement furthermore.

4.3. Risk Lover

What the mainstream macro-economists supporting the IS-LM model ignores is this psychological characteristics of economic agents the risk loving attitude toward investment.

When the macroeconomic level of the aggregate income goes down during either the policy tightening or the recession, these risk loving investors start investing more in order to compensate for their loss by the downturn. Even though their action notably increases, they tend to be willing to invest a lot for increase the nominal investment return furthermore.

Their prior objective is to maximise the gross income growth despite the high risk reducing the average expected investment return. So, they will either maintain the current investment volume or even increase the volume in spite both the investment risk, the high central bank interest rate, and the high tax and/or the less government expenditure.

In particular during the economic bubble, an euphoria severely affects people's mind enough to lose their rationality. So, they often tend to become the risk lovers while the economic bubble.

5. Risk Premium in case of the Perfect Competition

Even in the Perfect Competition Model fails in the real investment mechanism because it ignores the interest rate influenced by the risk premium of investment. When renders invest, they add the extra interest rate charge on the top of the risk free interest rate which the mainstream economists supporting the IS-LM model use in the macroeconomic model.

The graph indicates the interest rate setting of a bank under the monopoly:

Under the monopoly or a less competitive market, these firms simply takes the cost incurred by the investment risk by spiriting the expense from their profit.

By contrast, in the perfect competition, it is very complicated to explain with only the saving=investment curves so that the graph will be a overly complicated mess if it attempts to explain the risk premium rate setting under the perfect competition.

So, this analysis introduces the cost denoted as C, which indicates the cost of attracting savers, the interest payment to the central bank, and then the risk premium all together.

The graph below sets the saving motive and the central bank interest rate as rigid so that takes account of only the investment motive and the risk premium.

In this case, the interest rate is not guaranteed to be counter-cyclical to the business cycle, and it can be acyclical or even possibly pro-cyclical to the business cycle.

Some economists argue that the risk premium factor may affect the investment cost more than the other factors such as the central bank interest rate, the saving ratio, and the aggregate income/productivity level.

So, the final interest rate influencing the investment volume may rather rise during the recession because the risk premium rises meanwhile the rate may fall due to the lower risk premium during the stable or booming period.